This morning at Apple’s special event in the Steve Jobs Theater at Apple Park, Vice President of Apple Pay Jennifer Bailey took the stage to announce Apple Card. These “Apple” name prefixes are growing tedious, but Apple Card is looking to reduce the tedium which permeates the credit card industry. Apple is championing its credit card as a new industry leader in a variety of areas, including privacy, security, transparency, lack of fees, and fair interest rates. Apple Card gives rewards in cash rather than points, and these “Daily Cash” rewards are distributed to your Apple Cash account every day. If Apple Card can deliver on its promises, it shows real potential to be a disruptor in the often exploitative credit card industry.

Posts tagged with "apple pay"

Apple Card: The MacStories Overview

iOS 12 AR Quick Look Demos→

I recently came across a demo of AR Quick Look, an iOS 12 feature that allows apps to present 3D and AR previews for objects built using the new USDZ file format. Shopify, the popular e-commerce platform, is going to take advantage of AR Quick Look to let customers preview items in their surroundings directly from Safari, contextually to the shopping experience.

Here’s Daniel Beauchamp, writing on the Shopify AR/VR blog:

For the past three years, Shopify has been exploring how AR / VR will change the way consumers shop. Last year, we showed how Apple’s ARKit could be used to provide compelling AR commerce experiences. The main complexity was that ARKit needed to be run in an app. This meant that Shopify merchants looking to offer these experiences had to have their own unique mobile apps that customers would need to download.

With iOS 12’s AR Quick Look, 3D models of products in the usdz file format can be uploaded directly to online Shopify stores and viewed in AR right within Safari, without needing to download a separate app.

His video gives you an even better idea of the integration possible between Safari, ARKit, and Apple Pay in iOS 12:

Beauchamp argues that “the web is how AR becomes mainstream” – looking at these demos, it’s hard to disagree. Not having to install a dedicated ARKit app for every single online store we use and actually having the ability to share and preview models from Safari or Messages is going to remove a ton of friction from the current ARKit experience (as far as shopping is concerned). I can imagine that producing 3D objects at scale will be merchants’ biggest hurdle in the short term, though.

I wasn’t aware of this until I did some research, but Apple also launched an interactive AR Quick Look Gallery as part of their ARKit 2 mini-site. You can also test Shopify’s improved shopping flow featuring ARKit and Apple Pay here.

Apple Publishes Video Promoting the Use of Face ID with Apple Pay

Following on the heels of last week’s video highlighting the power of Face ID as a way to unlock the iPhone X, today Apple released an ad promoting the technology’s use with its Apple Pay service. The new video follows in last week’s tongue-in-cheek footsteps.

Set to Back Pocket by Vulfpeck, the ad follows a young man as he walks through a crowded market. He sees a hat he likes, uses Face ID with Apple Pay to buy it, and the hat flies off the rack and onto his head. Next, he does the same thing with a pair of sunglasses he likes. From there, he uses Face ID and Apple Pay to try on a dizzying array of shirts, suits, and shoes. He even buys a chair as a gift that rockets away leaving a trail of flame. Like the video last week, the ad is fun and does a nice job of conveying how Apple Pay works and how easy it is to use, while also being entertaining.

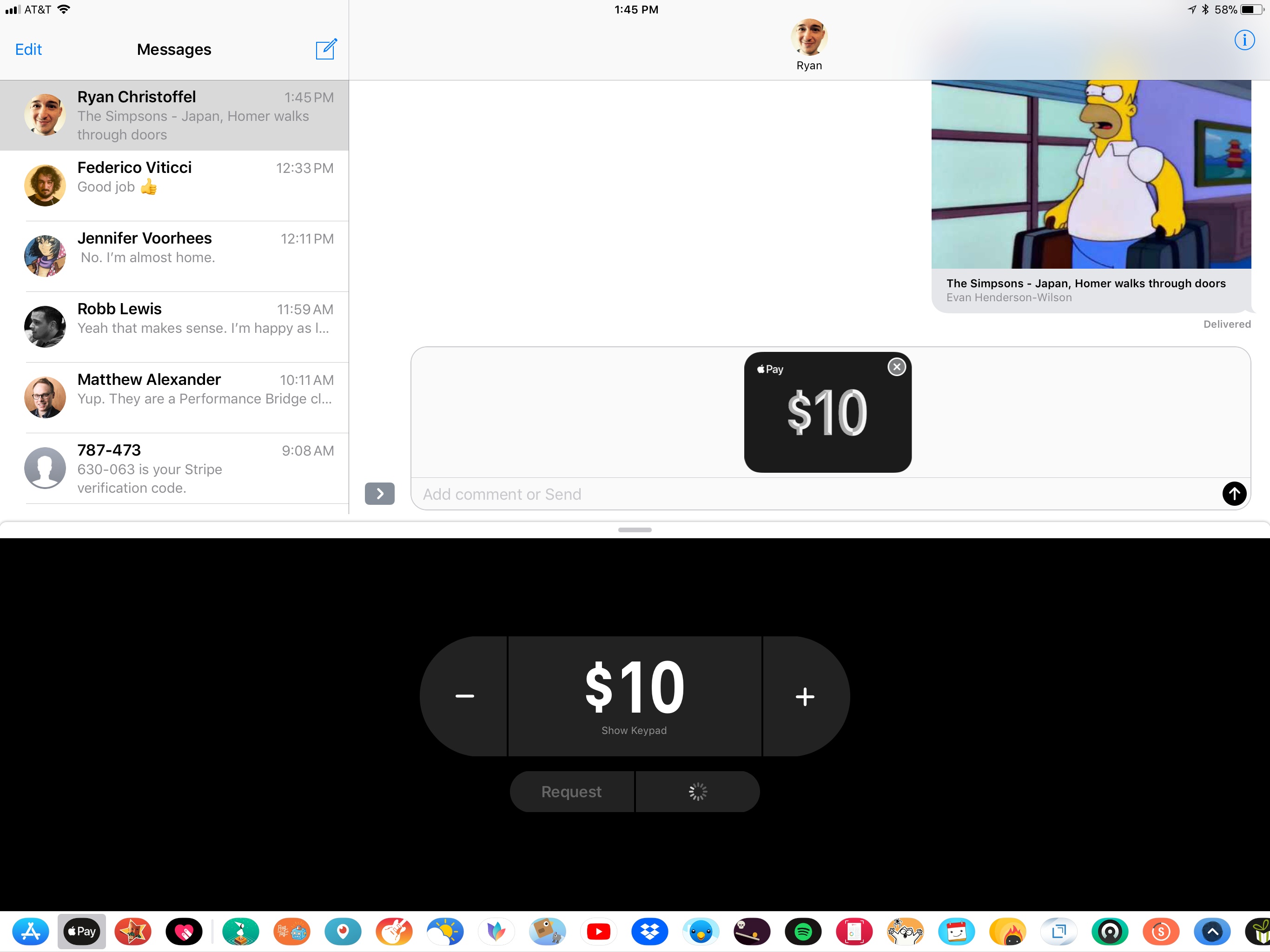

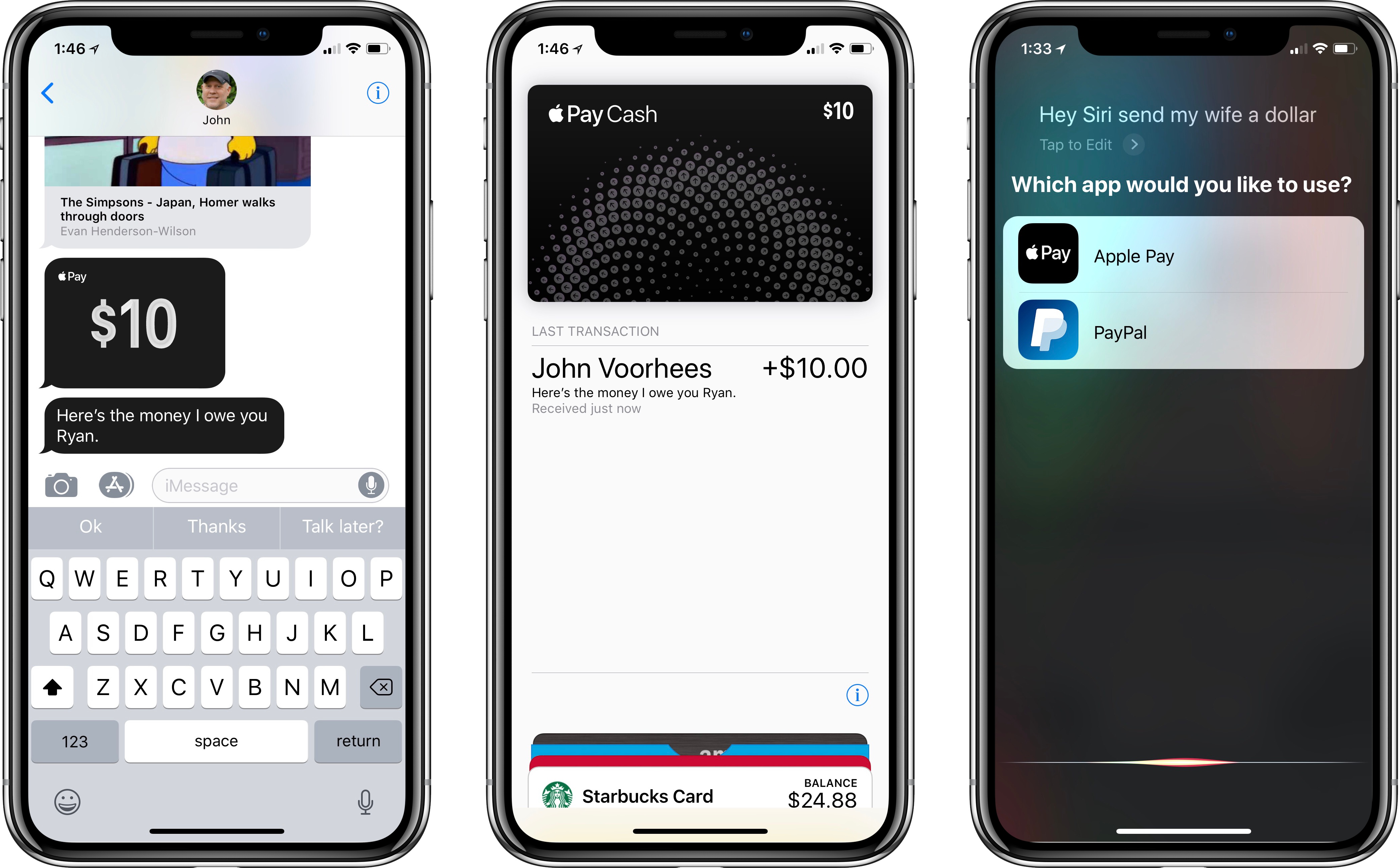

Apple Pay Cash Rolls Out in the US to iOS 11.2 Users

Last weekend Apple issued an update to iOS 11 that fixed a bug that could cause an endless loop of crashes if certain notifications were received by a user. Version 11.2 of iOS also set the stage for the rollout of Apple Pay Cash, Apple’s peer-to-peer money transfer service that’s built into the Messages app.

Apple Pay Cash is currently a US-only service that lets users send each other cash via iMessages. An Apple Pay button will appear in the app and sticker tray of Messages on any Apple Pay-compatible iPhone or iPad. The service, which debuted at WWDC in June and was previously available only to beta testers of iOS 11.2, includes integration with Siri. Messages also automatically suggests using Apple Pay Cash if money is mentioned in a text message.

If the service is tied to a debit card, there is no fee to send money to someone. However, users who use a credit card will be charged a 3% fee. There is also a $3000 limit on individual transactions and a $10,000 limit on sending or receiving funds within a seven-day period.

Apple Pay for iMessage Debuts in iOS 11.2 Beta

Users of the latest iOS 11.2 beta release received a surprise today in their Messages app picker: the long-awaited Apple Pay iMessage app has now arrived.

Apple Pay’s Expansion and Apple Pay Cash→

At the Money 20/20 conference earlier this week, Jennifer Bailey, Apple’s VP of Apple Pay, revealed some new stats about the service and announced an expansion to four new major markets. Ingrid Lunden has the full story at TechCrunch, but this part about Apple Pay Cash (the peer-to-peer payment feature announced at WWDC that hasn’t launched yet) stood out to me:

When Apple Pay Cash is turned on, for example, it will operate like Venmo, allowing users to transfer money quickly to each other via iMessage, Siri and other channels — a service that “thousands” of Apple employees are now already using in a closed beta before the service is turned on more widely later this year in an iOS 11 update.

But in addition to that, users will also be able to take that money and spend it directly at retailers and others that accept Apple Pay.

So you’ll not only be able to send money to other people over iMessage, but Apple Pay Cash will effectively be its own card that can be used at any physical store or website that supports Apple Pay (like our own Club). I’m intrigued.

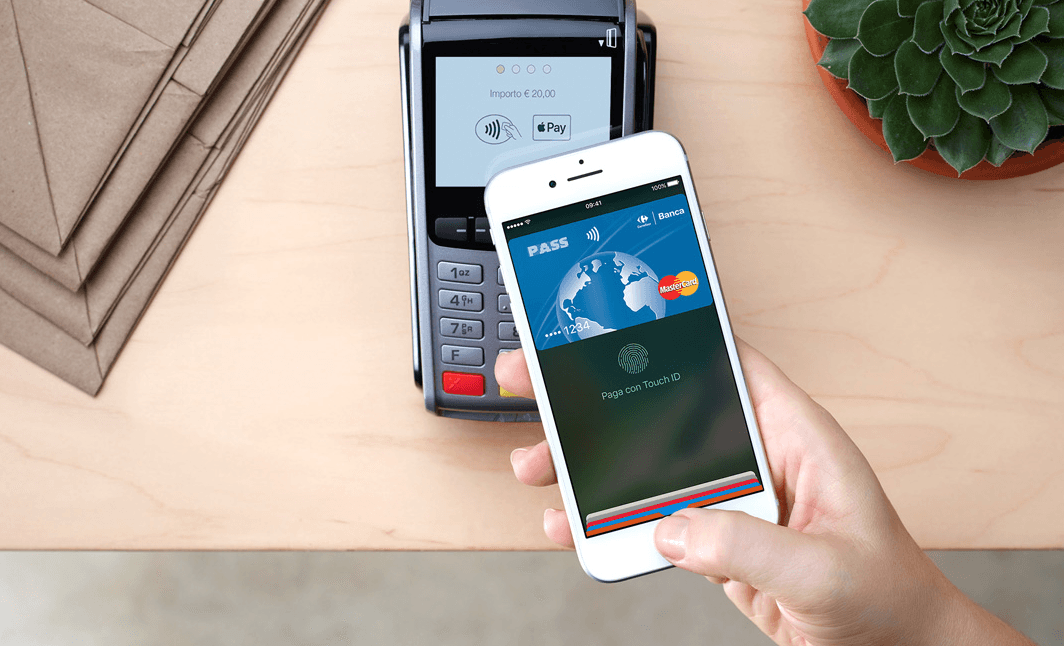

Apple Pay Debuts in Italy

Apple Pay continued its global expansion today adding three Italian banks, Carrefour Banca, Unicredit, and Boon. Each financial institution’s credit and debit cards can be added to Apple Pay and used in a variety of retail shops and with online retailers. The addition of Italy to the list of countries with Apple Pay support had been widely anticipated since March when the payment service was first listed as ‘Coming Soon’ to Italy. In total, Apple Pay is now available in 16 countries worldwide.

Later this year, more financial institutions will be added to Apple Pay in Italy. According to Apple’s Italian Apple Pay website, American Express, CartaBCC, ExpendiaSmart, Fineco Bank, Hype, Mediolanum Bank, N26, and Widiba will be adding Apple Pay support. The site also lists some of the major retailers that have signed up to accept Apple Pay in Italy, including H&M, Eataly, Auchan, Carrefour, Simply Market, OVS, Limoni, Sephora, Esselunga, and others.

Apple Pay Launches in Ireland, Coming Soon to Italy→

Benjamin Mayo, writing for 9to5Mac:

As we reported exclusively last night, Apple Pay is now live in Ireland. The service allows iPhone and Apple Watch owners to use the NFC chips in their devices to pay for their shopping at contactless terminals in retail stores across the country.

Apple Pay requires iPhone 6, iPhone 6s, iPhone SE, iPhone 7, or any Apple Watch, and is launching with support for Ulster Bank and KBC in Ireland. Apple has also announced that the service is coming soon to Italy.

I’ve been waiting for Apple Pay to launch in Italy, and I’m glad to see Apple has confirmed the service will roll out “soon”. However, as I feared, my bank – despite being one of the largest banking groups in Italy – is not going to be supported at launch. This has happened with 14 other countries (including Ireland) before, though, and I hope Apple will quickly get other major Italian banks on board.